The Biggest Mistakes Sellers Are Making Right Now

The housing market is going through a transition. Higher mortgage rates are causing more moderate buyer activity at the same time the supply of homes for sale is growing.And if you aren’t working with an agent, you may not realize that. Here’s the downside. If you’re not informed, you can’t adjust y

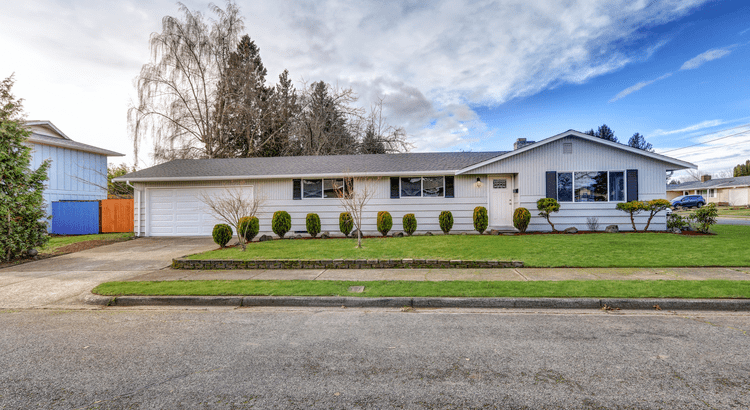

The Longer a home sits, the less it sells for

How To Find the Best Deal Possible on a Home Right Now Want to know how to find the best deal possible in today’s housing market? Here’s the secret. Focus on homes that have been sitting on the market for a while. Because when a listing lingers, sellers tend to get more realistic – and, more willing

Case-Shiller Index: San Diego home prices continue downward trend

A house is for sale in San Carlos area. (File photo by Chris Stone/Times of San Diego) The closely-watched Case-Shiller Index of national home prices shows a continued decline in San Diego amid a “new equilibrium of minimal price growth.” The latest report, released just before Thanksgiving, showed

Categories

- All Blogs (47)

- Advertising (3)

- AI (1)

- Apartments (1)

- Buying (16)

- Compensation (1)

- Condo (1)

- Construction (1)

- Development (1)

- Dining (1)

- DOJ (1)

- Downtown San Diego (2)

- Escrow (1)

- Expired (1)

- Fees (5)

- Food (1)

- Home Projects (1)

- Housing Market (15)

- Infographics (1)

- Inventory (7)

- Investment (1)

- Listing (2)

- Little Italy (1)

- Marketing (4)

- Mortgage Rates (9)

- National Association of Realtors® (NAR) (3)

- Negotiation (4)

- Ocean Beach (1)

- Podcast (1)

- Price (14)

- REALTOR® (5)

- Restaurants (1)

- San Diego (1)

- Seaport San Diego (1)

- Seaport Village (1)

- Second Home (1)

- Selling (21)

- Showing (2)

- Statistics (1)

- Technology (1)

- VA Loans (2)

- Website (1)

- Zillow (1)

Recent Posts